Top 8 things to know about the new Blended Retirement System

By Maj. Michael Odle

Defense Department assistant director of military compensation policy

Download

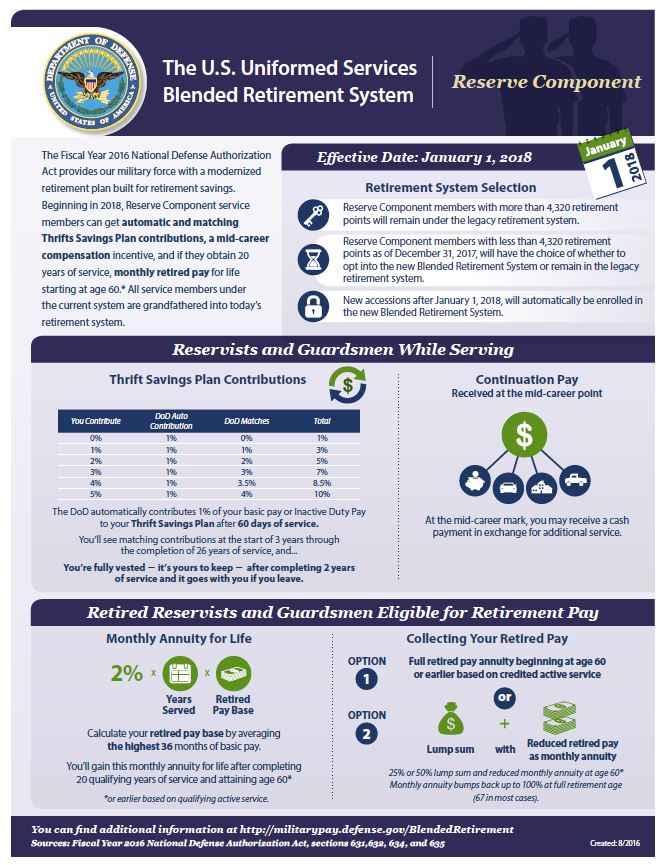

The National Defense Authorization Act for Fiscal Year 2016 created a new military retirement system that blends elements of the legacy retirement system with a more modern, 401(k)-style plan. The new Blended Retirement System goes into effect on Jan. 1, 2018.

Following are the top 8 things you should know about the new retirement system.

1. The new Blended Retirement System covers more people.

About 85 percent of service members who enter the military will receive some form of a government retirement benefit; whereas today only about 19 percent of service members receive monthly retired pay after at least 20 years of service.

2. You will be able to receive up to five percent employer contributions to your TSP.

Service members currently have the option of putting their money into the Thrift Savings Plan, but unlike their government civilian counterparts, they don’t receive matching government contributions. That changes under the Blended Retirement System. Soldiers, Sailors, Marines and Airmen who opt in will now receive an automatic one percent Department of Defense (DoD) contribution starting after 60 days, and DoD matching up to four percent of their basic pay at the start of their third year of — for up to five percent in government contributions. Both the DoD automatic one percent and the matching contributions continue through 26 years of service. One thing to note, current service members who opt into the Blended Retirement System in calendar year 2018 will receive the DoD automatic one percent and up to four percent additional DoD matching contributions immediately, without waiting two years.

3. Greater portability of retirement benefits for those who don’t intend to stay 20 years.

For decades, service members have had to serve 20 years before becoming eligible for monthly retired pay. Because about 81 percent of military personnel leave the service before 20 years, most service members leave without any government retirement benefit. However, under the Blended Retirement System, service members are vested after two years of service — the money in the TSP belongs to them, including all DoD automatic and matching contributions. If a service members leaves, the TSP goes with them.

4. The new plan has a trade-off.

For those who retire after at least 20 years of service, the retirement remains predominantly a defined benefit in which the service member will still get monthly retired pay. But if you choose the new plan, instead of monthly retired pay being calculated at 2.5 percent times the average of the service member’s highest 36 months of basic pay, as is done under the current retirement plan, the service member’s monthly retired pay will be calculated with a two percent multiplier.

5. If you joined after 2005 and want to opt into the new system, it must be done in 2018.

Everyone who is currently serving in the military as of Dec. 31, 2017, will be grandfathered under the legacy retirement system and nobody will be automatically moved to the new Blended Retirement System. However, Reserve Component service members with less than 4,320 retirement points as of Jan. 1, 2018, will have the choice of whether to stay with the legacy retirement system or opt into the new Blended Retirement System. Eligible service members will have until Dec. 31, 2018, to make a decision on which retirement system is right for them.

6. DoD continuation pay adds incentive for commitment of four more years.

The National Defense Authorization Act also included a continuation pay provision as a way to encourage service members to continue serving. Continuation pay is a direct cash payout, like a bonus. When a service member reaches 12 years of service, Active Component members will be eligible for a cash incentive of 2.5 to 13 times their regular monthly basic pay, and Reserve Component members will be eligible for 0.5 to six times their monthly basic pay (as if serving on active duty) in return for a commitment of four more years of service to Uncle Sam. It’s up to the individual services to determine who gets what, but it will likely be based on service needs.

7. New lump-sum option gives choices at retirement.

The lump-sum option allows service members to choose to elect 25 percent or 50 percent of their discounted retired pay in exchange for a reduction in monthly retired pay until the service member reaches full Social Security retirement age, which for most is 67 years old. At full Social Security retirement age, the service member would begin receiving their full monthly retired pay again. The DoD continues to work on guidance related to this valuable new option for service members. Stay tuned.

8. Education about the new retirement plan is key.

The DoD has initiated an 18-month, multi-stage financial education training curriculum to prepare active-duty and Reserve Component members and their Families. These courses will be available on Joint Knowledge Online and select courses will be available through Military OneSource. Read more about the mandatory training for eligible service members here.

Final thoughts. There is no single right answer as to which retirement system is better. Both the legacy retirement system and the Blended Retirement System may have advantages and disadvantages, based on a service member’s particular circumstances. Bottom line: Those service members who have the option of choosing their retirement system should base their decision entirely upon their own circumstances, after completing the training and taking advantage of all of the information and resources available. Educating yourself about the new retirement plan is key. |